Mortgage Protection Overview

Your home is one of your biggest investments, and protecting it is key to securing your family’s future. This overview will help you understand what Mortgage Protection Insurance is, why it is important, and how we can help you find the perfect coverage.

What Is Mortgage Protection Insurance

Mortgage Protection Insurance is designed to help protect your family and your home if something unexpected happens to you. If you pass away while coverage is in force, the policy pays a death benefit to your beneficiaries. This benefit can be used to help pay off the mortgage or keep payments current so your loved ones are not forced to sell the home during a difficult time.

Mortgage protection is not designed to protect the lender. It is designed to help protect your family, your equity, and the life you have worked hard to build.

Mortgage Protection Insurance vs Private Mortgage Insurance

Mortgage Protection Insurance is often confused with Private Mortgage Insurance, but they serve very different purposes.

Private Mortgage Insurance protects the lender if you stop making payments. It does not pay benefits to your family and does not help them keep the home.

Mortgage Protection Insurance is designed to protect your family. If you pass away, your beneficiaries will receive a benefit they control and can use toward the mortgage or other essential expenses.

How Mortgage Protection Insurance Works

You choose a coverage amount based on your mortgage balance, monthly payment, or financial goals. If you pass away while the policy is active, your beneficiaries receive a lump sum death benefit. They may use this benefit to pay off the mortgage entirely or continue making payments while they stabilize financially.

For example, a $2,000 monthly mortgage combined with a $50,000 benefit could cover approximately twenty-five months of payments.

Coverage is flexible and can be customized to your individual situation.

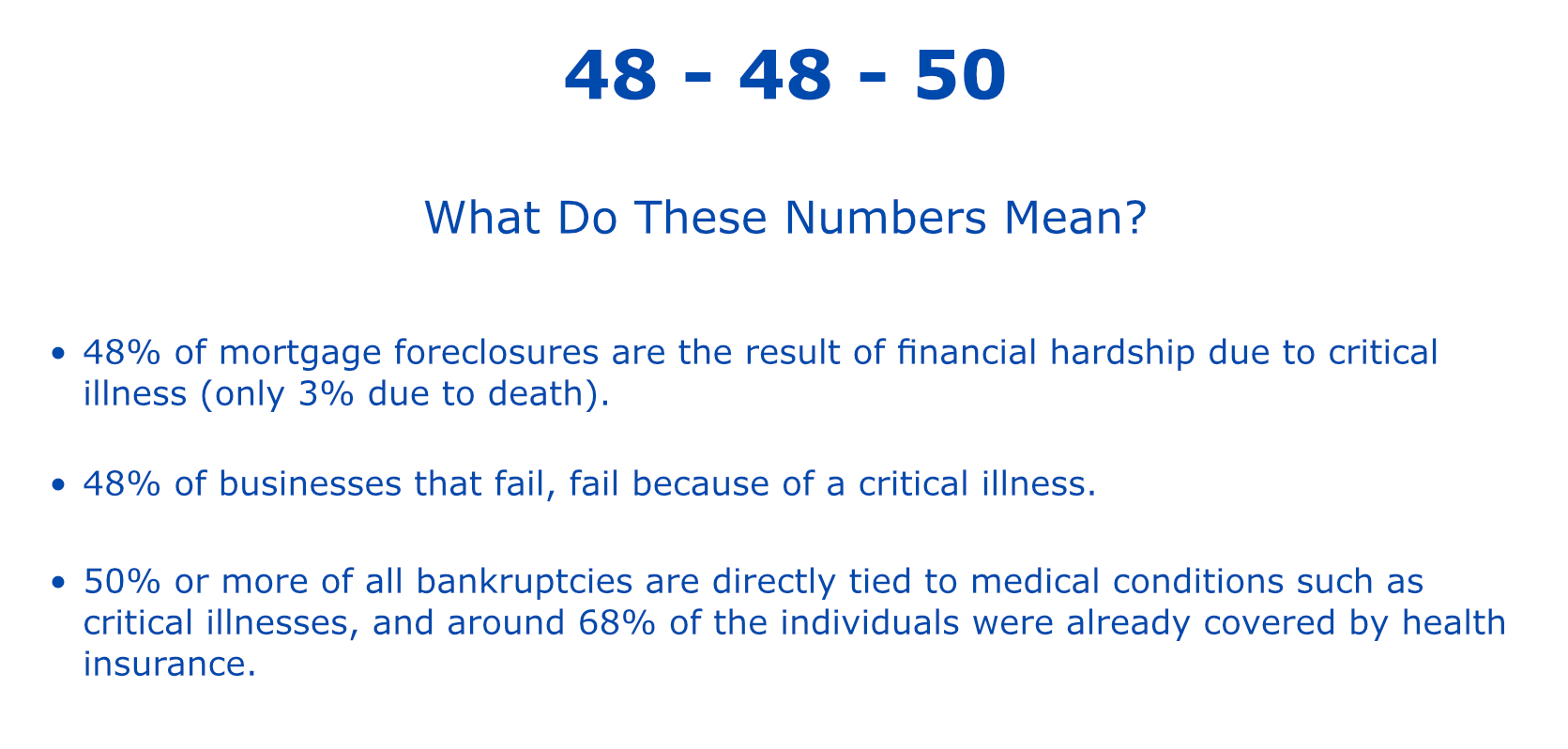

Health Risks That Make Mortgage Protection Essential

Significant health issues can disrupt your ability to earn income and make mortgage payments. Consider the following statistics:

- Stroke affects approximately 800,000 people each year, with an estimated 80% survival rate.

- Heart attacks impact about 795,000 individuals annually, with roughly a 90% survival rate.

- Cancer affects 1 in 2 men and 1 in 3 women during their lifetime, with survival rates varying by type and stage.

Mortgage protection helps ensure that even in the face of serious and unexpected health challenges, your home and family may remain financially secure.

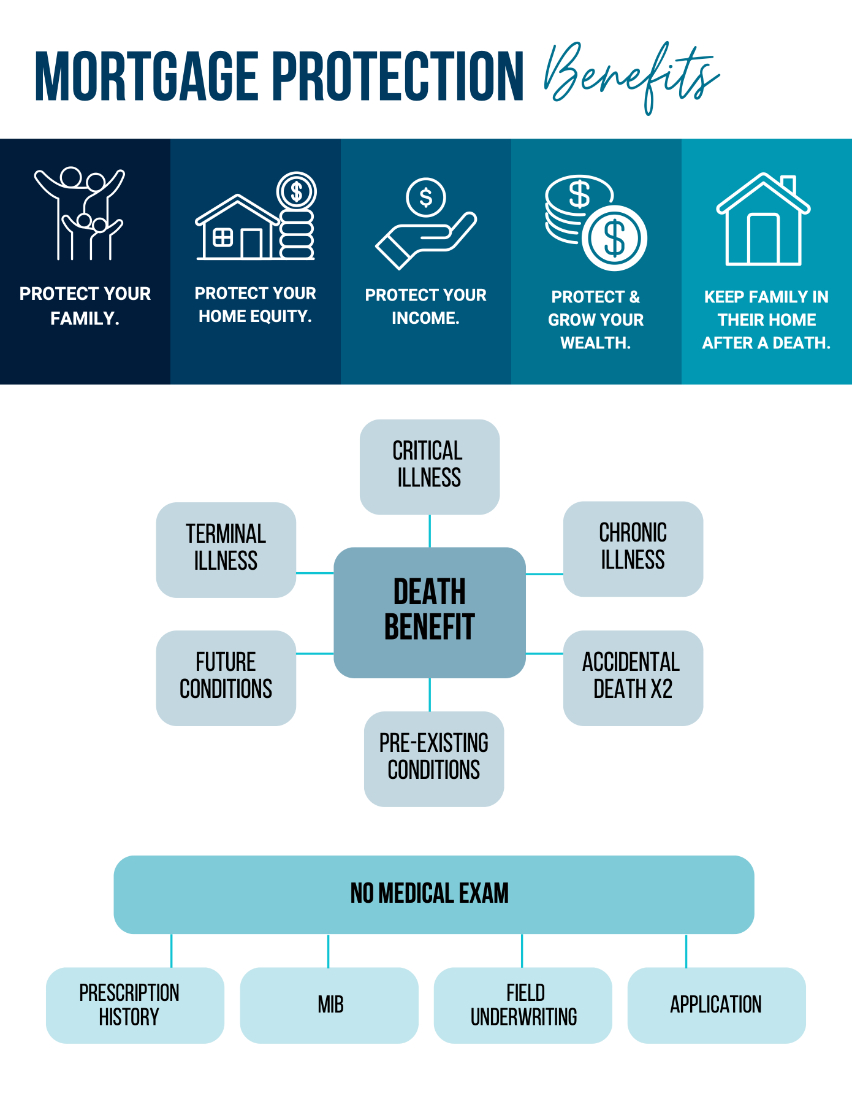

Living Benefits May Be Available

Some mortgage protection policies may include Accelerated Death Benefit riders, commonly referred to as living benefits. If included and if you qualify, these riders may allow early access to a portion of the death benefit in certain situations, subject to carrier approval.

Critical Illness

This rider may provide an accelerated death benefit if you are diagnosed with a qualifying condition, such as a heart attack, stroke, cancer, ALS, major organ failure, or kidney failure that prevents you from working.

Chronic Illness

If you are unable to perform at least two of the six Activities of Daily Living for a continuous period of ninety days, such as bathing or dressing, and this is certified by a physician, this benefit may provide early access to policy funds.

Terminal Illness

This rider may provide an accelerated death benefit if you are diagnosed with a life expectancy of twelve months or less.

Life insurance death benefits are generally income tax-free. Accessing benefits early may reduce the remaining death benefit. Please consult a tax professional for guidance regarding your specific situation.

These benefits may provide a financial cushion during life’s most difficult moments and offer meaningful peace of mind when it is needed most.

Types of Life Insurance Used for Mortgage Protection

Mortgage protection is commonly structured using life insurance. The most common options include the following:

Term Life Insurance

Term life insurance provides coverage for a specific period of time, such as ten, twenty, or thirty years. It is often chosen to match the length of the mortgage and typically offers lower premiums.

This option is best suited for homeowners who want affordable coverage for a defined time period.

Permanent Life Insurance

Permanent life insurance is designed to last for your lifetime and may include cash value features depending on the product. This option can provide long-term protection beyond the mortgage years.

This option is best suited for homeowners who want coverage that does not expire and additional financial flexibility.

Final Expense Insurance

Final expense insurance is a smaller permanent policy designed to help cover end-of-life costs. It may be used as a supplement, but generally not intended to replace full mortgage coverage.

Why Homeowners Choose Mortgage Protection

Homeowners choose mortgage protection for the clarity, stability, and peace of mind it provides during uncertain times. Key benefits include:

-

Security for Loved Ones: Surviving spouses and children are less likely to be left struggling with mortgage payments or forced into rushed financial decisions.

-

Built-in Flexibility: Beneficiaries can use the funds in the way that best supports their immediate needs.

-

Equity Preservation: Home equity is protected, and the risk of foreclosure may be reduced during periods of serious illness, disability, or loss of income.

-

Proactive Planning: Instead of leaving loved ones to navigate complex financial choices under stress, mortgage protection helps create a clear plan.

Mortgage protection is not about predicting the future; it is about being prepared for it.

How to Qualify for Coverage

Many mortgage protection policies are “simplified issue,” meaning no medical exams are required. Here is how the process works:

1. Health & Lifestyle Questionnaire: You start by answering a short series of health and lifestyle questions.

2. Electronic Underwriting: Insurance carriers electronically review prescription history, Medical Information Bureau (MIB) records, and driving history to evaluate eligibility.

3. Determination: Based on this quick review, the carrier determines approval, coverage options, and final pricing.

What Happens During a Mortgage Protection Coverage Review

During your coverage review, we focus on clarity and options, not pressure. We will discuss your mortgage, family goals, health profile, and budget. We then compare options from A-rated carriers and explain what you qualify for. If you choose to move forward, we will handle the application process.

Get Your Free Mortgage Protection Coverage Review

Protect your home. Protect your family. Protect what matters most.

Schedule your free 15-minute Mortgage Protection Coverage Review today to explore your options and see what you qualify for.